Take advantage of a shifting market! The Federal Reserve's recent rate drop is a game-changer for Chester County home buyers and sellers alike.

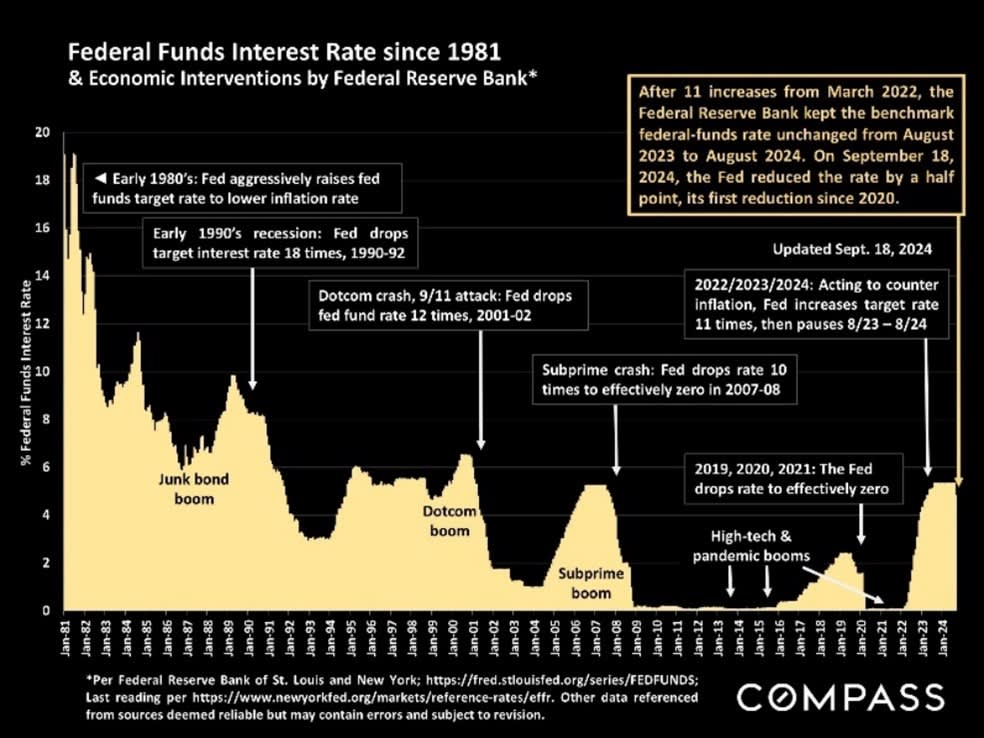

Over the past few weeks, headlines praising the Federal Reserve Bank (FED) and heralding a new wave of financial possibilities have been flooding economic media outlets. From claims of political motivation to praise for yet-to-be-seen results, the pundits have been going wild with this news. Here at COMPASS, we’ve had our own share of mixed responses, though the opening line of this month’s national real estate market insights captures a more neutral tone:

“On September 18th, the Federal Reserve Bank dropped its benchmark rate for the first time since 2020, and many analysts expect further cuts before the end of the year.”

-COMPASS National Real Estate Insights, September 2024

In My Own Words

With rate cuts like this, we have a window of opportunity for buyers and sellers alike to be the early bird and catch the worm. We know there is an opening now, and these opportunities don’t last long. Those buyers who have done their homework are ready and shopping, while sellers who have been waiting are bringing their homes to the market.

For example, we saw similar activity last November as mortgage companies reduced rates regardless of the FED’s rates. During that time, we saw a feeding frenzy of real estate activity across Chester County. It didn’t last long, though, before the winter holiday hubbub saw our real estate market freeze in place.

Before we get too much further, it’s worth mentioning that the FED impacting real estate activity isn’t exactly news. Just last month, I wrote an article about how the real estate market in our area was already bouncing back before this rate cut. Rather than looking at where the FED’s rate changes impacted us these past few years, let’s look at the past 10 months.

Join me as I figure out just how much these rate cuts could impact your wallet.

Working with Real Numbers

To really highlight how the FED’s rate change will impact you right now, let’s work through some examples. We’ll look at where the market was 5 years ago, last November, last May, and just this month since the FED’s rate drops. We’ll look at what you’d pay for a $400,000 mortgage, as well as an 80% loan-to-value (LTV) mortgage on the median sale price from that time period. Finally, we’ll compare the costs to you on a monthly, annual, and lifetime basis with your mortgage in these scenarios.

Back in November, Freddie Mac set their rates at 7.76%. Just a few months later, in May when the spring market was in full swing, Freddie Mac was down to 7.02%. And as of September 19th of this year, just a few days after the FED reduced their rates, we saw mortgage rates of 6.09% from Freddie Mac, the lowest they’ve been since Feb 2, 2023.

Let’s look at what your monthly payments would look like on a $400,000 loan at those different rates.

Example 1: Monthly Payments

|

Time Period |

Interest Rate* |

Loan Amount |

Monthly Payments |

|

November 2023 |

7.76% |

$400,000 |

$2,868.41 |

|

May 2024 |

7.02% |

$400,000 |

$2,666.58 |

|

September 19, 2024 |

6.09% |

$400,000 |

$2,421.40 |

Example 2: Annual Payments

|

Time Period |

Interest Rate* |

Loan Amount |

Annual Payments |

|

November 2023 |

7.76% |

$400,000 |

$34,420.96 |

|

May 2024 |

7.02% |

$400,000 |

$31,999.02 |

|

September 19, 2024 |

6.09% |

$400,000 |

$29,056.75 |

Example 3: Lifetime Payments

|

Time Period |

Interest Rate* |

Loan Amount |

Lifetime Payments |

|

November 2023 |

7.76% |

$400,000 |

$1,032,628.90 |

|

May 2024 |

7.02% |

$400,000 |

$959,970.57 |

|

September 19, 2024 |

6.09% |

$400,000 |

$871,702.57 |

*Per Freddie Mac at https://www.freddiemac.com/pmms.

What does it all mean for me?

After all that, you may be saying to yourself “sure, Jon, those are some charts. What does it actually mean for me, though?” Well, let’s look at the real-world impact these numbers have on your wallet.

|

Time Period |

Monthly Payment per $1000 Borrowed |

Monthly Payment for a $400,000 Mortgage |

Annual Payment for a $400,000 Mortgage |

Lifetime Payments for a $400,000 Mortgage |

|

Nov 2023 |

$7.17 |

$2,868.41 |

$34,420.96 |

$1,032,628.90 |

|

May 2024 |

$6.67 |

$2,666.58 |

$31,999.02 |

$959,970.57 |

|

Sep 2024 |

$6.05 |

$2,421.40 |

$29,056.75 |

$871,702.57 |

Wow, buyers paid a whopping $7.17 per thousand dollars borrowed last November during the real estate mini-frenzy!

Amount Saved Getting a Mortgage September 19, 2024, vs

|

Time Period |

Amount Saved Per Month |

Amount Saved Per Year |

Amount Saved in 30 Years |

|

Nov 2023 |

$447.01 |

$5,364.12 |

$160,926.33 |

|

May 2024 |

$245.18 |

$2,942.16 |

$88,268.00 |

This table clearly shows how buyers in today’s market are saving huge compared to the November market of last year, and are saving over $200 a month compared to those who purchased at the same price point just 4 months ago. For those who have been waiting for an opportunity, I can’t imagine a clearer signal.

Conclusion

With the first FED rate cut in 4 years, now is a golden opportunity in real estate. Mortgage rates are dropping faster than we’ve seen in years. Home values are more stable in our area than we’ve seen since the pandemic. And all that works out to conditions that are too good to last.

I hope this opportunity doesn’t pass you by. You deserve to live in the home you want and need, and market conditions are finally lining up to let people like you make moves. Housing inventory remains low, and these golden conditions are sure to keep changing. While I can’t predict what next month, let alone next year, will bring, I can see that opportunity is knocking today.